News Update – September 2019:

The Government has just announced that it will delay the introduction of VAT Reverse Charging by a year after it was heavily criticised for rushing through the changes without consultation with trade bodies and organisations in the Construction Industry. Implementation will now be delayed until 1 October 2020.

Our original update as follows:

Introducing reverse charge VAT for the Construction Industry

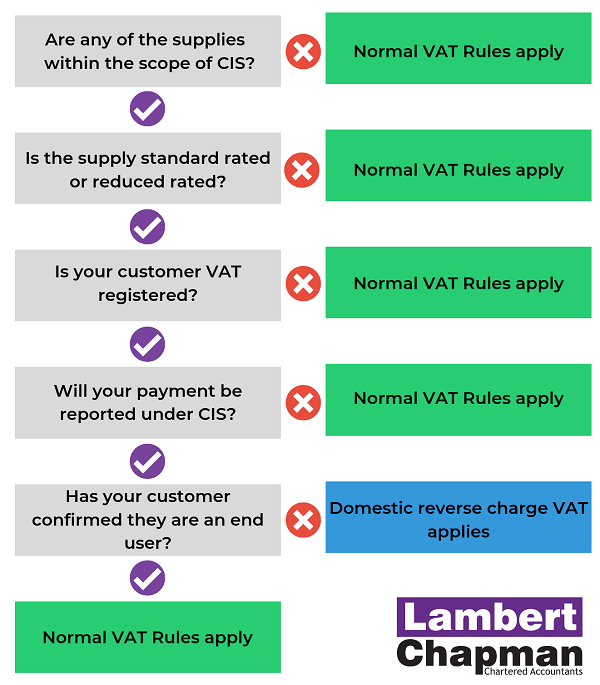

What is the reverse charge?

- The services are supplied to an end user (e.g. the property owner) or directly to a main contractor that sells or lets a newly completed building

- The recipient of the services is not VAT registered, or required to be VAT registered

- The recipient is not registered for the CIS

- The supplier and recipient are landlord and tenant or vice versa, or

- The supplies are zero-rated, such as work on new residential property.

When to use the reverse charge legislation

How to prepare for reverse charge VAT

If you supply services under the construction industry scheme, the Revenue recommends you take these steps to prepare before 1 October 2019.

Construction businesses will need to ensure their accounting systems are capable of processing reverse charge transactions and make ongoing checks to ensure that supplies and purchases are correctly treated. As the VAT amount must still be shown on invoices subject to the domestic reverse charge, there is a clear risk that suppliers will pay the VAT over to HMRC in error and similarly customers will reclaim it in error.

Subcontractors that rely on VAT collected from their customers as working capital until they have to pay it to HMRC, potentially four months later, are likely to suffer from the loss of cash flow. These businesses will need to consider if payment terms need to be renegotiated to avoid problems.

Services affected by the reverse charge

The reverse charge for VAT applies if your VAT-registered business supplies constructing, altering, repairing, extending, demolition or dismantling services.

This applies to buildings, structures, walls, roadworks, power lines, electronic communications equipment, aircraft runways, railways, inland waterways, docks and harbours.

For a comprehensive list of services that are affected by the reverse charge for VAT, go to GOV.UK

Critics round on HMRC

The construction industry had been expecting the guidance to be released 12 months before the change takes effect and the Revenue has been criticised for the way it has implemented the reverse charge, particularly the amount of time it has taken to issue the detailed guidance.

If you require any further information or guidance, please arrange to speak to myself or your usual Lambert Chapman contact.

Posted by Mike Carabine

Disclaimer

The views expressed in this article are the personal views of the Author and other professionals may express different views. They may not be the views of Lambert Chapman LLP. The material in the article cannot and should not be considered as exhaustive. Professional advice should be sought in connection with any of the issues contained in the article and the implementation of any actions.