We are all aware that putting money into a pension enables us to save for our future retirement but have you considered the savings that are available now?

Each year, we all have up to £40,000 of annual allowance for pension contributions. If you are an employee, these can be made by you and/or your employer.

If you are not working, you can still make a net contribution of £2,880 (or a grandparent could make a gift), on which your pension pot will receive a refund from the Government of 20%. Making the total contribution £3,600.

Owner/Director – Low Salary

Do you own your own company? Take a small salary and some dividends each year? How about getting your company to make pension contributions?

As a director, your company may not be required to register for Auto Enrolment so there may not be a requirement to make pension contributions but they could still make payments into your personal pension or SIPP. Irrespective of your net relevant earnings, the company could make contributions of up to £40,000 in this tax year. These are fully deductible for corporation tax purposes and are a tax efficient way of releasing funds from the business.

It is important to note that HM Revenue and Customs may question why the pension contributions are higher than your salary.

Individual – High Income

As an individual with

Once income, including pension

If higher contributions are made, then there is a pensions charge, declarable on your Self Assessment Tax Return, on the excess at 45%. If this tax exceeds £2,000 then you can ask your pension fund to pay the tax on your behalf. You may consider from a commercial standpoint that if your employer is making the contributions, that this is still a benefit, as long as the lifetime allowance is not at risk.

As an employee, one option would be to consider salary sacrifice. This means giving up some of your salary in

Unused Allowances

If you have been making pension contributions in earlier years but not using the full allowances available to you, how about making a ‘catch-up’ payment?

Is it possible to make use of unused allowances for the current and prior 3 tax years so 2018/19, 2017/18, 2016/17 and

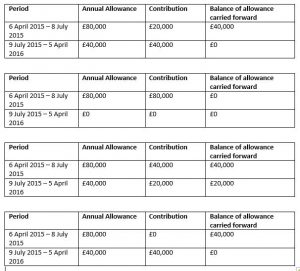

2015/16 is a special year for pension annual

We would need to review your contribution records to determine whether you have any carry forward from 2015/16 but it is possible that a significant amount could be available and lost if not used by 5 April 2019. Please note that contributions are allocated against the current year allowances first so contributions in excess of £40,000 may be required to access this earlier year relief.

Subject to further investigations, you could have the following allowances available to use:

2015/16 – £40,000

2016/17 – £10,000 to £40,000

2017/18 – £10,000 to £40,000

2018/19 – £10,000 to £40,000

Total – £70,000 to £160,000

Notes:

- Net relevant earnings – income from a trade; employment income; taxable redundancy payment and benefits

- Auto Enrolment – Employer minimum contribution – 2% to 5 April 2019, 3% thereafter.Total minimum contribution – 5% to 5 April 2019, 8% thereafter

- Lifetime Allowance – £1,030,000 from April 2018 with inflationary rise due in April 2019

- This is just a brief overview of the rules and your own specific position should be reviewed separately.

If you wish to discuss making a pension contribution before the 5 April 2019, please contact Lucy

Disclaimer

The views expressed in this article are the personal views of the Author and other professionals may express different views. They may not be the views of Lambert Chapman LLP. The material in the article cannot and should not be considered as exhaustive. Professional advice should be sought in connection with any of the issues contained in the article and the implementation of any actions.